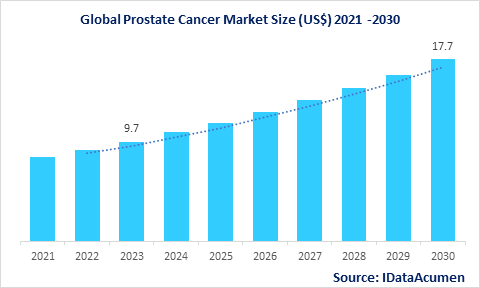

The Prostate Cancer Market is poised for significant growth, with projections indicating a surge in its size from US$ 9.7 billion in 2023 to a robust US$ 17.7 billion by 2030. This anticipated expansion reflects a remarkable compound annual growth rate (CAGR) of 8.9% during the forecast period.

Prostate cancer, a prevalent malignancy affecting men worldwide, is characterized by the abnormal proliferation of cells within the prostate gland, ultimately resulting in the development of tumors. The treatment landscape for this disease encompasses various modalities such as radiation therapy, surgical interventions, chemotherapy, hormone therapy, and immunotherapy, providing a spectrum of options for patients. The escalating global incidence of prostate cancer stands out as a pivotal driver propelling the growth trajectory of this dynamic market.

Prostate cancer, a prevalent malignancy among men globally, involves the abnormal growth of cells in the prostate gland, leading to tumor formation. Treatment options encompass radiation therapy, surgery, chemotherapy, hormone therapy, and immunotherapy, providing a spectrum of choices for patients. The escalating global incidence of prostate cancer serves as a primary driver propelling the market's growth, highlighting the need for continued research and development in this field to address this pervasive health concern.

Epidemiology Insights:

- Prostate cancer is the second most common cancer in men globally, with around 1.4 million new cases and 375,000 deaths estimated in 2020. It accounts for 7.3% of all cancer cases in men.

- In the US, prostate cancer is the most prevalent cancer in men, with around 250,000 new cases and 34,000 deaths estimated in 2021. 1 in 8 men will be diagnosed with prostate cancer during their lifetime.

- In Europe, around 450,000 men were diagnosed with prostate cancer and 107,000 died from the disease in 2020. The UK, Norway, Ireland, Belgium, and Iceland have the highest incidence rates.

- Japan has witnessed rapidly rising prostate cancer incidence, from 32.7 cases per 100,000 males in 2008 to 51.3 cases per 100,000 in 2016. This growth is attributed to dietary changes, screening, and the aging population.

- Developing regions like Latin America, the Middle East, and Africa have lower incidences, but the rates are projected to rise significantly over the coming decade.

Market Landscape:

- Current treatment options like chemotherapy, hormone therapy, radiation, and surgery are effective but have considerable side effects. There is a need for better tolerated therapies.

- Leading therapies include Zytiga, Xtandi, Jevtana, Provenge, Xofigo, etc. Key drug classes are LHRH agonists, anti-androgens, taxanes, immunotherapy, radio-pharmaceuticals, etc.

- Emerging advances include precision medicine, focal therapy with HIFU/cryotherapy, therapeutic cancer vaccines, PARP inhibitors, novel hormone drugs, and biomarker testing.

- Immune checkpoint inhibitors have shown potential in early trials, with drugs like Keytruda, Opdivo, and Bavencio being evaluated. These can significantly disrupt the market landscape.

- The market is dominated by patented drugs from major pharma companies like Johnson & Johnson, Pfizer, Astellas, AstraZeneca, etc. Generics have limited penetration currently.

Prostate Cancer Market Drivers:

Increasing Prevalence of Prostate Cancer

Prostate cancer is one of the most commonly diagnosed cancers in men globally. According to research, the prevalence of prostate cancer has increased significantly over the past decade. Some key factors attributing to this rising prevalence include the aging population, sedentary lifestyles, and unhealthy diets. The surging number of prostate cancer cases is creating huge demand for various treatment options like radiation therapy, chemotherapy, immunotherapy, hormonal therapy, etc. This rising patient pool is a major factor driving the growth of the prostate cancer therapeutics market.

Advancements in Early Diagnosis and Screening

Several advanced diagnostic tests have been developed in recent years for early and accurate diagnosis of prostate cancer. These include the prostate-specific antigen (PSA) blood test, digital rectal exam (DRE), MRI scan, biopsy, genomic testing, etc. PSA screening has become very common for prognosis of prostate cancer. Early diagnosis is critical for better treatment outcomes. The increasing adoption of regular screening and diagnosis protocols among men, especially those in high-risk groups, is significantly contributing to market growth.

Development of Targeted Therapies

Extensive R&D by biopharma companies has led to targeted therapy emerging as a key treatment approach for prostate cancer. Targeted drugs can specifically act on cancer cells while minimizing damage to normal cells. Prominent examples include hormone therapies like LHRH agonists and anti-androgens, PARP inhibitors like Lynparza, Olaparib, Rucaparib, and radio-pharmaceutical drugs like Xofigo. The launch of such innovative therapeutic agents that improve survival rates and quality of life is driving the market potential.

Favorable Reimbursement and Government Funding

Prostate cancer therapies are often expensive, especially advanced treatments like immunotherapy and robotic surgery. Favorable reimbursement coverage and financial assistance programs offered by governments in developed countries like the US and Europe help patients afford these cutting-edge treatments. Government funding for prostate cancer research also enables rapid development of novel therapeutics. Such favorable policies and initiatives are boosting the adoption of the latest prostate cancer drugs and devices.

Prostate Cancer Market Opportunities:

Rising Potential of Immunotherapy

Immunotherapy is an emerging treatment approach that utilizes the body's immune system to identify and attack cancer cells. Checkpoint inhibitor drugs that target proteins like PD-1/PD-L1 have shown promising results in clinical studies for metastatic castration-resistant prostate cancer (mCRPC). Keytruda, Opdivo, Bavencio, and other immuno-oncology drugs have potential in prostate cancer treatment. Positive clinical data and approvals will make immunotherapy a major disruptor in this market.

Increasing Adoption of Robot-assisted Surgery

Robot-assisted surgical systems like the da Vinci system offer minimally invasive prostatectomy and reduced risk of impotence/incontinence. Robotic surgery provides precision, flexibility, and quicker recovery. The wider availability of robotic surgical systems and surgeon experience with this technology is driving adoption for prostate cancer resection. Robotic surgery is expected to gain significant share in the prostate cancer market.

Emergence of Nanomedicine

The use of nanoparticles and other nanotechnologies for precision drug delivery to tumor sites can improve targeting and lower toxicity of chemotherapies. Nanoparticle-based therapeutics, diagnostic agents, and drug delivery systems for prostate cancer have huge potential. Companies are investing significantly in R&D in this area. Approval of nano-therapies with superior efficacy and safety can disrupt the prostate cancer market.

Growth Opportunities in Emerging Markets

Developing countries in Asia, Latin America, Middle East, and Africa offer significant opportunities for growth owing to expanding healthcare infrastructure and rising healthcare expenditure. Increasing prostate cancer incidence, improving diagnosis rates aided by medical tourism, and growing adoption of advanced therapies in these emerging markets will contribute to the market growth. Local manufacturing, partnerships, and differentiation strategies can help tap the potential.

|

Key Insights |

Description |

|

The market size in 2023 |

US$ 9.7 Bn |

|

CAGR (2023 - 2030) |

8.9% |

|

The revenue forecast in 2030 |

US$ 17.7 Bn |

|

Base year for estimation |

2021 |

|

Historical data |

2017-2020 |

|

Forecast period |

2023-2030 |

|

Quantitative units |

Revenue in USD Million, and CAGR from 2021 to 2030 |

|

Market segments |

By Treatment Type: Hormone Therapy, Chemotherapy, Immunotherapy, Targeted Therapy, Surgery, Radiation Therapy, Others By End User: Hospitals, Cancer Research Institutes, Ambulatory Surgical Centers, Others By Distribution Channel: Hospital Pharmacies, Retail Pharmacies, Online Pharmacies By Stage: Localized, Locally Advanced, Metastatic, Castration-Resistant By Region: North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

|

Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East, and Africa |

|

Market Drivers |

|

|

Market Restraints |

|

|

Competitive Landscape |

Johnson & Johnson, Pfizer, Astellas Pharma, AstraZeneca, Bayer, Bristol Myers Squibb, Novartis, Roche, Merck, Ipsen, AbbVie, Sanofi, Ferring Pharmaceuticals, Takeda, Teva Pharmaceutical, Janssen Biotech, Clovis Oncology, Myovant Sciences, GSK, Eli Lilly |

Prostate Cancer Market Trends:

Personalized Medicine and Biomarker Testing

Personalized medicine that utilizes pharmacogenomics and biomarker testing for tailored treatment plans based on the patient's genetic profile is a major trend in prostate cancer management. For instance, FoundationOne® liquid biopsy test identifies biomarkers like BRCA1/2 mutations that can guide targeted therapy selection. The launch of more biomarker-specific drugs and companion diagnostics will drive personalized medicine adoption.

Advent of Focal Therapies

Focal therapy is an emerging minimally invasive approach suited for low and intermediate-risk localized prostate cancer. It uses precisely targeted ablative energy to eradicate small tumors while preserving surrounding tissues and minimizing side effects. Focal laser ablation, HIFU therapy, cryoablation, and other techniques are being evaluated as alternatives to radical prostatectomy. Focal therapies are expected to gain more acceptance in early-stage prostate cancer treatment.

Combination Therapies

Combining drugs from different classes such as hormonal therapy, immunotherapy, and chemotherapy is being explored as a promising treatment strategy for improving efficacy. For example, clinical trials have shown enhanced survival benefits with combination regimens like ADT plus docetaxel or ADT plus abiraterone acetate over individual drugs. More combination treatments will likely be adopted going forward.

Advances in Radiopharmaceuticals

Radioactive drugs like Xofigo that deliver targeted radiation to prostate cancer tissues represent an innovative category. Advances like prostate-specific membrane antigen (PSMA) targeted radioligands such as Pluvicto show enhanced antitumor activity with less toxicity. Several radiopharmaceutical candidates are progressing through late-stage trials. Next-gen radio-drugs are poised to gain share.

Prostate Cancer Market Restraints:

High Cost of Targeted Therapies

Novel advanced targeted drugs and immunotherapies like Xtandi, Erleada, Nubeqa, Lynparza, and Pluvicto used for metastatic and late-stage prostate cancer treatment are expensive, sometimes exceeding USD 10,000 per month. The high cost can be prohibitive for many patients, especially where reimbursement coverage is limited. This impedes therapy adoption and market growth.

Adverse Effects of Treatment

Radiation therapy, hormone therapy, chemotherapy, and surgery used for prostate cancer treatment can negatively impact quality of life, leading to urinary/sexual dysfunction, fatigue, weakness, gastrointestinal problems, etc. Fear of such adverse effects deters patients from compliance with prescribed therapies, thereby restricting market growth and opportunity.

Low Screening Rates in Developing Countries

Lack of awareness on prostate cancer screening and diagnosis protocols for high-risk individuals persists in developing regions. Limited access, high costs, social stigma, and inadequate public health policies inhibit PSA testing adoption. This leads to later diagnosis at advanced stages when treatment is less effective. Lags in early screening threaten market expansion.

Recent Developments:

|

Development |

Involved Company |

|

FDA approval of Pluvicto |

Novartis |

|

Health Canada approval of Nubeqa |

Bayer |

|

FDA approval of Erleada for high-risk non-metastatic CSPC |

Johnson & Johnson |

|

Launch of Onureg for mCRPC |

Pfizer |

|

FDA approval of Rubraca for BRCA mutation mCRPC |

Clovis Oncology |

|

CHMP positive opinion for Jemperli in mCRPC |

GSK |

|

Lynparza Phase 3 PROpel trial meets primary endpoint |

AstraZeneca |

|

European approval of Xtandi for Pfizer |

Astellas mHSPC

|

Key Product Launches:

- Pluvicto approval in March 2022 was the first PSMA-targeted radioligand therapy for prostate cancer. It can treat mCRPC cases with PSMA-positive metastases and provides better survival benefit.

- Nubeqa (darolutamide) approved in June 2022 is an oral androgen receptor inhibitor for nmCRPC. In the ARASENS trial, it showed a significant improvement in metastasis-free survival.

- Erleada received expanded FDA approval in September 2021 for treatment of patients with high-risk non-metastatic castration-sensitive prostate cancer based on Phase 3 data demonstrating improved overall survival.

Regional Analysis:

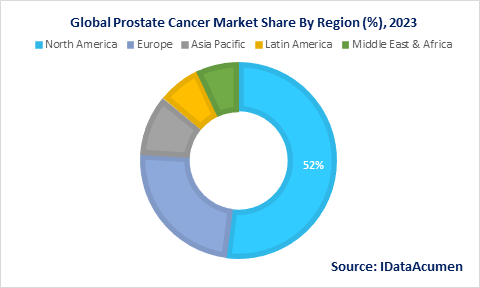

In 2023, North America emerged as the dominant hub for the prostate cancer market, commanding a substantial share of over 52% in global revenues. This commanding position is attributable to a combination of factors, including a high level of awareness about prostate cancer, widespread access to screening and diagnostic facilities, the availability of cutting-edge treatments, and robust healthcare spending within the region.

Meanwhile, Europe accounted for approximately 24% of the market share in the prostate cancer landscape in 2023. This significant presence can be attributed to the widespread adoption of prostate-specific antigen (PSA) screening initiatives and an increasingly aging population. Notably, key European markets driving this share include Germany, France, and Italy, where prostate cancer awareness and research efforts have made notable strides.

Looking ahead, the Asia Pacific region is poised for remarkable growth, anticipated to exhibit the highest growth rate with a CAGR of 9.5% between 2023 and 2030. Currently, Japan and China are prominent players in this regional market, driven by their large populations and growing healthcare infrastructure. Furthermore, emerging economies such as India, Korea, and Australia are opening up significant opportunities within the prostate cancer market, fueled by increasing healthcare awareness and access, making Asia Pacific a focal point for future market expansion.

Prostate Cancer Market Segmentation:

- By Treatment Type

- Hormone Therapy

- Chemotherapy

- Immunotherapy

- Targeted Therapy

- Surgery

- Radiation Therapy

- Others

- By End User

- Hospitals

- Cancer Research Institutes

- Ambulatory Surgical Centers

- Others

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Stage

- Localized

- Locally Advanced

- Metastatic

- Castration-Resistant

- By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Top Companies in the Prostate Cancer Market:

- Johnson & Johnson

- Pfizer

- Astellas Pharma

- AstraZeneca

- Bayer

- Bristol Myers Squibb

- Novartis

- Roche

- Merck

- Ipsen

- AbbVie

- Sanofi

- Ferring Pharmaceuticals

- Takeda

- Teva Pharmaceutical

- Janssen Biotech

- Clovis Oncology

- Myovant Sciences

- GSK

- Eli Lilly