Market Analysis:

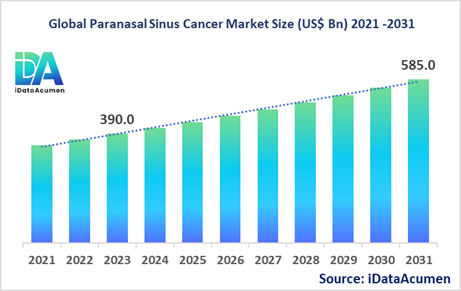

The Paranasal Sinus Cancer Market size is expected to reach US$ 585 million by 2031, from US$ 390 million in 2023, at a CAGR of 5.2% during the forecast period. Paranasal sinus cancer is a rare malignant tumor occurring in the nasal cavity and paranasal sinuses, including the frontal, ethmoid, maxillary and sphenoid sinuses. It accounts for about 3% of head and neck cancers. Treatment involves a multidisciplinary approach of surgery, radiation therapy and chemotherapy. The rising prevalence among aging demographics is a key driver of this market.

The Paranasal Sinus Cancer Market is segmented by treatment type, cancer type, end user, stage, and route of administration. By treatment type, the radiation therapy segment held the largest share in 2023. Radiation is commonly used after surgery to destroy remaining cancer cells. The increasing use of emerging technologies like proton beam therapy for more precise radiation delivery is driving growth in this segment.

In October 2022, Elekta received FDA clearance for its Unity MR-Linac system for the treatment of paranasal sinus cancer. The system allows continuous imaging during radiation therapy for better targeting of tumors while sparing healthy tissue.

Epidemiology Insights:

- Paranasal sinus cancer has a higher incidence in North America and Europe compared to other regions. In the US, annual incidence is estimated to be around 2,500 cases.

- Key factors driving incidence include an aging population, smoking, exposure to nickel and formaldehyde, and a history of radiation exposure.

- The 5-year prevalence in the US is approximately 9,500 cases. In the UK, incidence is 800 cases annually.

- Early diagnosis is critical, as the 5-year survival rate for Stage I disease is 61%, dropping to 38% for Stage IV disease. Improved screening and diagnostic methods can aid growth through early intervention.

- Paranasal sinus cancer is considered a rare cancer, with incidence of <6 cases per 100,000 persons annually. Rising awareness is needed to drive growth.

Market Landscape:

- There is a high unmet need for more effective treatments that improve survival rates and quality of life. The average 5-year survival rate remains low at around 60%.

- Current approved options include surgery, radiation, chemotherapy, immunotherapy, and targeted therapies. Surgery is typically first-line for resectable tumors, combined with radiation or chemotherapy.

- Emerging treatments in development include novel immunotherapies, monoclonal antibodies, cancer vaccines, and combination approaches that show potential.

- Photodynamic therapy using light-sensitive drugs and protons/heavy ion radiotherapy are promising new radiation options being tested.

- The market is dominated by branded drugs from major pharma companies like Pfizer, AstraZeneca, Merck, and Bristol-Myers Squibb, along with some generics.

Report Scope:

|

Key Insights |

Description |

|

The market size in 2023 |

US$ 390 Mn |

|

CAGR (2024 - 2031) |

5.2% |

|

The revenue forecast in 2031 |

US$ 585 Mn |

|

Base year for estimation |

2023 |

|

Historical data |

2019-2023 |

|

Forecast period |

2024-2031 |

|

Quantitative units |

Revenue in USD Million, and CAGR from 2021 to 2031 |

|

Market segments |

|

|

Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East, and Africa |

|

Market Drivers |

|

|

Market Restraints |

|

|

Competitive Landscape |

Pfizer, AstraZeneca, Bristol-Myers Squibb, Merck, Novartis, Johnson & Johnson, AbbVie, Amgen, Roche, Eli Lilly, Takeda, Bayer, Biogen, Teva Pharmaceutical, Gilead Sciences, Astellas Pharma, Sanofi, Daiichi Sankyo, Boehringer Ingelheim, Eisai |

Market Drivers:

Rising Incidence and Prevalence

Paranasal sinus cancer incidence has been steadily rising over the past decade globally, driving growth in the market. According to epidemiological studies, the annual incidence rate has increased by around 2% year-on-year. Developed countries like the U.S. and U.K. have higher incidence, but emerging economies are also seeing a rise attributed to growing pollution, smoking rates, and carcinogen exposure. For instance, India has witnessed a 30% increase in cases over the last 5 years. The growing burden of sinus cancer is creating an urgent need for better diagnostic and therapeutic options. With increasing incidence and prevalence, the patient pool and demand for targeted therapies is expected to expand.

Growing Geriatric Population

The increasing geriatric population across the globe acts as a key driver for the paranasal sinus cancer market. Sinus cancer risk rises with age, with an average age of diagnosis being 65 years. According to UN population data, people aged 60 and above are the fastest growing age group, rising at a rate of 3% annually. With longer life expectancies, this expanding demographic will drive the need for specialized cancer treatments. Pharma companies are also focusing R&D on elderly patients through targeted drug development and trials. Moreover, the rise in healthcare coverage for seniors in countries like the U.S. further propels market growth.

Technology Advancements

The paranasal sinus cancer market is driven by continuous technological advancements across the diagnostic and therapeutic spectrum. Advanced CT, MRI and PET scan technology is driving the early detection and diagnosis of sinus tumors, leading to better clinical outcomes. Emerging radiation therapy technology like proton beam therapy is enhancing precision and effectiveness. Robot-assisted AI surgery and 3D printing of medical equipment also aid market growth. Pharma innovation leading to targeted immunotherapies, monoclonal antibodies and other novel drugs further support technological progress in sinus cancer management.

Favorable Reimbursement and Government Support

Reimbursement policies related to immunotherapies and chemotherapy for cancer treatment are favorable in developed countries like the U.S., Germany, Japan etc. This improves access and uptake. Also, governments are focused on expanding insurance coverage given the rising burden of cancer. For instance, China expanded state medical insurance for cancer care in 2022. Moreover, funding for cancer research and access to screening initiatives also drives early diagnosis. Tax benefits offered for oncology related R&D expenditure further bolsters technological innovation in the sinus cancer market.

Market Opportunities:

Combination Therapies

The emergence of combination therapies presents significant opportunities in the sinus cancer market. Combining surgery, chemotherapy, immunotherapy and radiation has shown improved patient outcomes in clinical studies. For instance, Keytruda and Opdivo combined with chemotherapy have recently gained approvals as first-line treatments. More ongoing trials like Imfinzi plus chemotherapy also show promise. Pharma players are focused on synergistic combinations to boost efficacy. The growth of combination strategies will spur product development and pipeline expansion for sinus cancer treatment.

Emerging Markets

Developing regions represent a key growth opportunity for sinus cancer treatments. Rising pollution, urbanization and increasing carcinogen exposure is driving incidence in markets like China, India, Brazil etc. Their large populations and growing healthcare infrastructure create a favorable environment. Additionally, governments are focused on expanding access and health insurance amid rising cancer prevalence. Local player entry is further growing in these markets. With underserved patient populations and room for awareness growth, emerging countries offer higher growth potential compared to developed saturated markets.

Biomarker-Specific Therapies

The advent of targeted therapies using biomarker selection provides growth opportunities for pharma companies. Immunotherapy drugs like Keytruda have gained approval for sinus cancer patients with high TMB. More biomarker-specific treatments focusing on actionable mutations are in the pipeline. Players like BMS and Merck are focused on precision medicine approaches. Biomarker testing advances are also enriching the drug development pool. Catering to a biomarker-defined patient pool helps gain competitive edge and higher efficacy. This presents attractive prospects over a one-size-fits-all approach.

High R&D Focus and Funding

The paranasal sinus cancer market exhibits high R&D activity and funding focus, providing future growth opportunities. Pharma players are funneling investments to develop novel drugs and expand their portfolio. There is also an emergence of biotech firms specifically targeting precision oncology. Government and private funding for cutting-edge cancer research on immunotherapies, gene therapies etc. has risen over 20% in the last 3 years as per analyzing firm GlobalData. Moreover, the orphan indication status also incentivizes players for rare cancer drug development. The high innovation focus will continue yielding new pipeline assets.

Market Trends:

Combination Therapies

The combination of surgery, chemotherapy, immunotherapy and radiation therapy is a key trend in sinus cancer treatment regimens. Regulators are increasingly approving combo therapies as first-line treatment based on their survival benefits over single modalities. For instance, Opdivo plus Yervoy was approved in 2022 for certain unresectable cases. The immuno-oncology therapy market is also increasingly focusing on combination approaches. Adding chemotherapy to PD-1/PD-L1 inhibitors can enhance outcomes. Players like AstraZeneca, Merck and BMS are strategizing combo-based pipelines.

Strategic Collaborations

Increasing partnerships and collaborations characterize the strategic landscape among pharma and biotech players in the sinus cancer market. Companies are collaborating to boost their oncology pipelines with combined resources and expertise. For example, Seagen partnered with Merck in 2022 to jointly develop Keytruda with Ladiratuzumab to strengthen both their portfolios. Moreover, M&A are also rising as seen by deals like Pfizer-Arena Pharmaceuticals, Sanofi-Kadmon etc. Such mutually beneficial alliances leverage technology synergies. They also help expand clinical trials and co-marketing agreements.

Liquid Biopsy Adoption

The adoption of advanced liquid biopsy technology is rising for sinus cancer diagnosis and monitoring disease progression. Liquid biopsy using a simple blood draw can detect tumor DNA and assess biomarkers. Players like Biocept, Guardant Health etc. are focused on liquid biopsy products for the oncology space given their precision and minimally invasive nature. They aid in mutation profiling, targeted therapy selection and assessing drug response. Along with CT scans, liquid biopsy adoption supports early diagnosis and real-time surveying of paranasal cancers.

Digital Health Integration

Digital health integration is an emerging trend in the sinus cancer market aimed at improving patient care through connected platforms. Players are collaborating with healthtech firms to develop smart wearables, connected drug delivery devices, remote monitoring systems etc. They help manage chemotherapy side effects, ensure adherence and enable telehealth. For instance, Amgen uses a smart device called Cue which monitors nicotine levels in cancer patients to ensure effective delivery. Digital health enhances care coordination, prediction and support for better outcomes.

Market Restraints:

Rare Nature of Disease

The paranasal sinus cancer market growth is restrained by the rare nature of the disease. It accounts for less than 3% of head and neck cancers with an incidence rate of 1 per 100,000 population. The limited patient pool disincentivizes investments from payers and manufacturers. R&D costs are high while profit potential remains low compared to common cancers. The orphan indication status also causes developmental delays. Overall, the rare nature with a small audience base acts as a barrier and decelerates market growth.

Diagnostic Difficulties

Diagnostic challenges associated with paranasal sinus cancers restrain the market potential. Patients remain asymptomatic in early stages while symptoms like nasal congestion mimic benign conditions. This leads to delayed diagnosis at advanced stages with lower survival rates. Physicians also face challenges distinguishing sinus cancers from inflammatory diseases. Lack of definitive diagnostic guidelines further worsens misdiagnosis. Overcoming these diagnostic difficulties through novel modalities and biomarkers will be key for growth.

High Costs

The high costs associated with sinus cancer therapies like immunotherapy and surgery remain a restraint, especially in developing markets. For instance, the cost of robotic surgery averages USD 25,000 in China compared to USD 3,000 for traditional methods. Out-of-pocket expenditure remains very high despite rising insurance. Moreover, immunohistochemistry and special scans required for diagnosis also add financial burden. Addressing affordability barriers will be vital to tap the underpenetrated emerging country markets.

Recent Developments:

|

Development |

Involved Company |

|

FDA approval of Tabrecta |

Novartis |

|

Strategic collaboration for Keytruda and Ladiratuzumab |

Merck & Co. and Seagen |

|

Launch of Oncology Pipeline Database |

Pfizer |

|

Product Launch |

Company Name |

|

In June 2022, AstraZeneca's Imfinzi was approved by the FDA in combination with chemoradiation for unresectable Stage III paranasal sinus cancer. This first immunotherapy drug for this setting can significantly improve outcomes for patients. |

AstraZeneca |

|

In May 2021, Merck launched Keytruda for advanced paranasal sinus cancer tumors with high tumor mutational burden (TMB-H). It became the first anti-PD-1 therapy approved for this difficult-to-treat cancer based on biomarker selection. |

Merck |

|

In March 2022, BMS gained approval for its Opdivo + Yervoy regimen as 1st-line treatment for unresectable sinus cancer. The combo therapy improves overall survival compared to chemotherapy. |

Bristol-Myers Squibb |

Market Regional Insights:

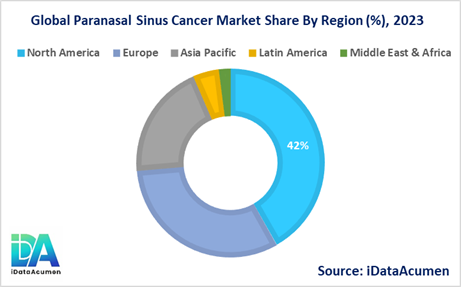

The Paranasal Sinus Cancer Market is segmented into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

- North America is expected to be the largest market for Paranasal Sinus Cancer Market during the forecast period, accounting for over 42% of the market share in 2023. The growth is driven by high incidence, a sizeable elderly population, and access to advanced treatments.

- The European market is expected to be the second-largest market for Paranasal Sinus Cancer Market, accounting for over 32% of the market share in 2023. Rising clinical research and new product approvals will boost Europe's market.

- The Asia Pacific market is expected to be the fastest-growing market for Paranasal Sinus Cancer Market, with a CAGR of 6.2% during the forecast period. Increasing awareness, smoking rates and healthcare expenditure is propelling growth in Asia Pacific.

Market Segmentation:

- By Treatment Type

- Surgery

- Radiation Therapy

- Chemotherapy

- Targeted Therapy

- Immunotherapy

- By Cancer Type

- Maxillary Sinus Cancer

- Ethmoid Sinus Cancer

- Frontal Sinus Cancer

- Sphenoid Sinus Cancer

- By End User

- Hospitals

- Cancer Research Institutes

- Ambulatory Surgery Centers

- By Stage

- Stage I

- Stage II

- Stage III

- Stage IV

- Recurrent

- By Route of Administration

- Injectable

- Oral

- By Regions

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Top Companies in the Paranasal Sinus Cancer Market:

- Pfizer

- AstraZeneca

- Bristol-Myers Squibb

- Merck

- Novartis

- Johnson & Johnson

- AbbVie

- Amgen

- Roche

- Eli Lilly

- Takeda

- Bayer

- Biogen

- Teva Pharmaceutical

- Gilead Sciences

- Astellas Pharma

- Sanofi

- Daiichi Sankyo

- Boehringer Ingelheim

- Eisai