Market Analysis:

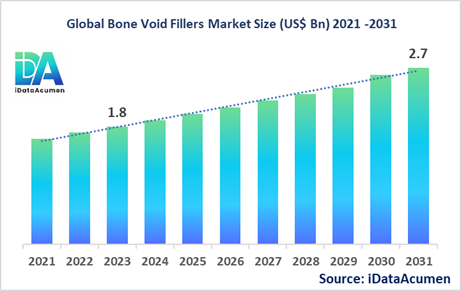

The Bone Void Fillers Market had an estimated market size worth US$ 1.8 billion in 2023, and it is predicted to reach a global market valuation of US$ 2.7 billion by 2031, growing at a CAGR of 5.2% from 2024 to 2031.

Bone void fillers are medical devices used to fill the spaces or voids in bones that can occur due to various reasons such as injuries, trauma, or surgical procedures. These materials help in the regeneration and healing of bone, providing structural support and facilitating the natural bone remodeling process.

The major drivers for the Bone Void Fillers Market include the increasing incidence of bone-related injuries and disorders, such as osteoporosis, leading to a growing demand for effective bone void filling solutions. Additionally, advancements in bone regenerative technologies and the rising adoption of minimally invasive surgical procedures have contributed to the market's growth.

The Bone Void Fillers Market is segmented by product type, application, end-user, material, and form. By product type, the market is segmented into synthetic bone graft substitutes, demineralized bone matrix (DBM), allografts, bone morphogenetic proteins (BMPs), and others. The synthetic bone graft substitutes segment is expected to dominate the market due to their increasing adoption and advancements in material science.

Epidemiology Insights:

The global burden of bone-related injuries and disorders, such as osteoporosis, continues to be a significant public health concern. In North America, the prevalence of osteoporosis is estimated to affect around 10 million individuals, with a higher incidence among the aging population. In Europe, the disease burden is also substantial, with approximately 27.6 million people living with osteoporosis.

The key epidemiological trends driving the Bone Void Fillers Market include the increasing incidence of bone fractures, particularly in the elderly population, as well as the growing prevalence of degenerative bone diseases. The aging population and sedentary lifestyles are contributing to the rise in bone-related disorders, creating a growing demand for effective bone void filling solutions.

In the United States, the incidence of osteoporosis-related fractures is estimated to be around 2 million cases per year, with a significant impact on healthcare costs and patient quality of life. Similarly, in the European Union, the annual number of osteoporotic fractures is projected to reach 3.5 million by 2025.

These epidemiological trends present significant growth opportunities for the Bone Void Fillers Market, as the need for innovative and effective bone regeneration solutions continues to increase, particularly in regions with aging populations and high incidences of bone-related disorders.

Market Landscape:

The Bone Void Fillers Market faces several unmet needs, as the current treatment options often have limitations in terms of efficacy, safety, and patient outcomes. While traditional bone grafting techniques, such as autografts and allografts, have been widely used, they are associated with donor site morbidity and limited availability.

The current treatment options in the Bone Void Fillers Market include synthetic bone graft substitutes, demineralized bone matrix (DBM), and bone morphogenetic proteins (BMPs). These products aim to provide structural support, facilitate bone regeneration, and improve patient outcomes. However, some of these treatments have been associated with complications, such as infection and immune rejection.

Upcoming therapies and technologies in the Bone Void Fillers Market include the development of advanced, biocompatible, and biodegradable materials for bone void filling. These innovative solutions are designed to enhance bone regeneration, reduce the risk of complications, and improve patient quality of life.

One breakthrough treatment option currently being developed is the incorporation of 3D printing technology in the manufacturing of customized bone void fillers. This approach allows for the creation of patient-specific implants that can be tailored to the individual's anatomy and bone defect, potentially improving the fit and integration of the bone void filler.

The Bone Void Fillers Market is relatively consolidated, with a few large players dominating the market, such as Medtronic, Stryker, and DePuy Synthes. These companies have a strong presence and offer a wide range of bone void filler products. Additionally, there are several smaller and specialized players that cater to specific market segments.

Market Report Scope:

|

Description |

|

|

The market size in 2023 |

US$ 1.8 Bn |

|

CAGR (2024 - 2031) |

5.2% |

|

The revenue forecast in 2031 |

US$ 2.7 Bn |

|

Base year for estimation |

2023 |

|

Historical data |

2019-2023 |

|

Forecast period |

2024-2031 |

|

Quantitative units |

Revenue in USD Million, and CAGR from 2021 to 2030 |

|

Market segments |

|

|

Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East, and Africa |

|

Market Drivers |

|

|

Market Restraints |

|

|

Competitive Landscape |

Medtronic plc, Stryker Corporation, DePuy Synthes (Johnson & Johnson), Zimmer Biomet Holdings, Inc., Evonik Industries AG, Integra LifeSciences Holdings Corporation, Baxter International Inc., Graftys, Arthrex, Inc., NuVasive, Inc., Wright Medical Group N.V., Curasan AG, ORthoPhor, Biocomposites Ltd., Heraeus Medical GmbH, Bone Solutions Inc., Exactech, Inc., Algipharma AS, TEKNIMED, Aap Implantate AG |

Market Drivers:

Increasing Prevalence of Bone-Related Injuries and Disorders

The rising incidence of bone-related injuries and disorders, such as osteoporosis, traumatic fractures, and degenerative joint diseases, is a significant driver for the growth of the Bone Void Fillers Market. The aging population, sedentary lifestyles, and the increasing burden of chronic conditions have contributed to the escalating number of individuals suffering from bone-related problems. For instance, according to the International Osteoporosis Foundation, approximately 200 million people worldwide are affected by osteoporosis, with the condition leading to over 8.9 million fractures annually. This growing patient pool has created a heightened demand for effective bone void filling solutions that can facilitate bone regeneration, support the healing process, and improve patient outcomes.

Advancements in Bone Regenerative Technologies

The Bone Void Fillers Market has witnessed significant advancements in the field of bone regenerative technologies, driving the development of innovative and more effective bone void filler products. Researchers and medical device companies have been actively exploring novel biomaterials, including synthetic bone graft substitutes, demineralized bone matrices, and bioactive ceramics, that can mimic the natural properties of bone and enhance the body's natural healing processes. These advanced materials offer improved biocompatibility, osteoinductive and osteoconductive properties, and enhanced integration with the surrounding bone tissue, leading to better patient outcomes and driving the adoption of bone void fillers in various orthopedic and dental applications.

Increasing Demand for Minimally Invasive Procedures

The growing preference for minimally invasive surgical procedures has also contributed to the expansion of the Bone Void Fillers Market. Patients and healthcare providers are increasingly seeking treatment options that offer reduced recovery time, less pain, and improved cosmetic outcomes. The development of injectable and less invasive bone void filler formulations, such as pastes, gels, and putties, has enabled surgeons to deliver these materials through smaller incisions, reducing the overall surgical trauma and allowing for faster patient rehabilitation. This trend has driven the adoption of advanced bone void fillers, as they can be seamlessly integrated into these minimally invasive surgical techniques, providing a more patient-centric approach to bone regeneration and healing.

Rising Healthcare Expenditure and Improved Access to Advanced Treatments

The Bone Void Fillers Market has also benefited from the overall increase in healthcare expenditure and the improved accessibility of advanced medical treatments, particularly in emerging economies. As healthcare systems in developing regions continue to evolve and invest in modern medical infrastructure, the availability and utilization of innovative bone void filler products have expanded. This trend is further supported by the increasing awareness among healthcare professionals and patients about the benefits of these specialized medical devices, leading to a higher adoption rate and driving the growth of the Bone Void Fillers Market.

Market Opportunities:

Expanding Applications in Dental and Craniomaxillofacial Procedures

The Bone Void Fillers Market presents significant growth opportunities in the dental and craniomaxillofacial domains. The increasing prevalence of dental implants, periodontal diseases, and maxillofacial trauma has created a rising demand for effective bone void filling solutions that can enhance bone regeneration and facilitate the integration of dental and facial prosthetics. Innovative bone void filler products, such as those with improved biocompatibility and the ability to promote vascularization, are being increasingly adopted in these specialized applications. For example, the use of synthetic bone graft substitutes in dental ridge augmentation and sinus lift procedures has gained traction, as they offer a reliable alternative to traditional bone grafting techniques.

Leveraging 3D Printing Technology for Customized Bone Void Fillers

The integration of 3D printing technology in the Bone Void Fillers Market presents a significant growth opportunity. By leveraging 3D printing, manufacturers can create customized bone void filler implants that are tailored to the patient's specific anatomical needs and bone defect characteristics. This personalized approach can improve the fit and integration of the implant, leading to better clinical outcomes and patient satisfaction. Additionally, 3D printing enables the production of complex and patient-specific bone void filler geometries, which can be challenging to achieve with traditional manufacturing methods. As 3D printing technologies continue to advance and become more accessible, the Bone Void Fillers Market is expected to witness increased adoption of these customized solutions, catering to the unique requirements of each patient.

Expansion into Emerging Markets

The Bone Void Fillers Market also presents growth opportunities in emerging markets, particularly in regions like Asia Pacific, Latin America, and the Middle East. These regions are characterized by rapidly improving healthcare infrastructure, increasing healthcare expenditure, and a growing awareness among healthcare professionals and patients about the benefits of advanced bone void filler products. As these markets continue to develop, the demand for innovative and effective bone regeneration solutions is expected to rise, creating new avenues for market expansion. Companies in the Bone Void Fillers Market can leverage their expertise, product portfolios, and strategic partnerships to penetrate these emerging regions and capture a larger share of the growing global market.

Collaborative Efforts for Product Development and Clinical Research

Opportunities also exist in the Bone Void Fillers Market through collaborative efforts between medical device companies, research institutions, and healthcare providers. These collaborations can drive the development of new and improved bone void filler products, as well as the conduct of comprehensive clinical research to establish the safety and efficacy of these solutions. By working together, stakeholders can leverage their respective strengths, knowledge, and resources to accelerate the innovation process, address unmet clinical needs, and enhance the overall understanding of bone regeneration therapies. Such collaborative initiatives can lead to the introduction of groundbreaking bone void filler technologies and contribute to the growth and advancement of the Bone Void Fillers Market.

Market Trends:

Increasing Focus on Biocompatible and Biodegradable Materials

The Bone Void Fillers Market is witnessing a growing trend towards the development and adoption of biocompatible and biodegradable materials for bone void filling applications. Researchers and medical device companies are actively exploring innovative biomaterials, such as synthetic polymers, ceramics, and composites, that can mimic the natural properties of bone and seamlessly integrate with the surrounding tissue. These advanced materials are designed to be gradually resorbed by the body over time, allowing for the gradual replacement with new, healthy bone. This trend is driven by the need to overcome the limitations of traditional bone grafting techniques and provide more effective and patient-friendly solutions for bone regeneration. As these biocompatible and biodegradable bone void fillers gain traction, they are expected to become the preferred choice for various orthopedic and dental procedures.

Integration of Advanced Imaging Technologies

The Bone Void Fillers Market is also experiencing a trend towards the integration of advanced imaging technologies, such as computed tomography (CT) and magnetic resonance imaging (MRI), to enhance the precision and effectiveness of bone void filler treatments. These advanced imaging techniques enable healthcare providers to accurately assess the size, location, and characteristics of bone defects, allowing for the selection and placement of the most appropriate bone void filler products. Moreover, the integration of 3D imaging and modeling capabilities has facilitated the development of customized bone void filler implants, further improving the fit and integration with the patient's unique anatomy. As these imaging technologies become more widely adopted in clinical settings, they are expected to drive the utilization of bone void fillers and improve overall patient outcomes.

Emphasis on Minimally Invasive Delivery Methods

The Bone Void Fillers Market is also witnessing a trend towards the development and adoption of minimally invasive delivery methods for bone void filler products. Healthcare providers and patients are increasingly seeking treatment options that offer reduced surgical trauma, shorter recovery times, and improved cosmetic outcomes. In response, medical device companies are focusing on the development of injectable and less invasive bone void filler formulations, such as pastes, gels, and putties, which can be delivered through smaller incisions or even percutaneously. These innovative delivery methods not only enhance the convenience and patient experience but also enable the integration of bone void fillers into emerging minimally invasive surgical techniques, further driving the growth of the Bone Void Fillers Market.

Emergence of Combination Therapies

The Bone Void Fillers Market is also experiencing the emergence of combination therapies, where bone void filler products are integrated with other advanced treatment modalities to enhance bone regeneration and healing. For instance, the incorporation of growth factors, stem cells, or other biological agents into bone void filler formulations is gaining traction, as these combination therapies have the potential to stimulate and accelerate the natural bone healing process. Additionally, the integration of bone void fillers with advanced scaffolding materials or drug-eluting technologies can provide a more comprehensive and tailored approach to address complex bone defects. As these combination therapies continue to evolve and demonstrate improved clinical outcomes, they are expected to become a prominent trend in the Bone Void Fillers Market.

Market Restraints:

High Cost of Advanced Bone Void Filler Products

One of the primary restraints in the Bone Void Fillers Market is the high cost associated with advanced bone void filler products. The development and manufacturing of these specialized medical devices, particularly those incorporating innovative biomaterials and cutting-edge technologies, can be resource-intensive. This often translates into higher prices for the end products, which can pose a significant barrier to adoption, especially in regions with limited healthcare budgets or reimbursement coverage. The high cost of bone void fillers can limit their accessibility and widespread use, particularly in certain patient populations or healthcare settings. This restraint underscores the need for continuous efforts to improve manufacturing efficiencies, streamline regulatory processes, and explore alternative financing mechanisms to make these advanced bone void filler solutions more affordable and accessible to healthcare providers and patients.

Regulatory Hurdles and Stringent Approval Process

The Bone Void Fillers Market is also subject to stringent regulatory requirements and a complex approval process, which can act as a restraint to the market's growth. Bone void filler products, as medical devices, must undergo rigorous clinical testing, safety evaluations, and regulatory approvals before they can be commercialized. This process can be time-consuming, resource-intensive, and pose challenges for both established players and new entrants in the market. The need to comply with evolving regulatory guidelines and obtain necessary approvals in multiple jurisdictions can delay the introduction of innovative bone void filler solutions, limiting the rate of market expansion. Navigating these regulatory hurdles requires significant investments in research, development, and clinical trials, which can further contribute to the high costs associated with these medical devices.

Limited Reimbursement Coverage for Bone Void Filler Procedures

The limited reimbursement coverage for bone void filler procedures is another significant restraint in the Bone Void Fillers Market. In many healthcare systems, the coverage and reimbursement policies for these specialized medical devices may not be comprehensive or may vary across different regions or payer organizations. This lack of consistent reimbursement can limit the adoption of bone void fillers, as healthcare providers and patients may be hesitant to incur the out-of-pocket expenses associated with these treatments. The absence of favorable reimbursement policies can particularly impact the utilization of more advanced and innovative bone void filler products, which tend to be more costly. Addressing this restraint through collaborative efforts with policymakers, payers, and healthcare stakeholders to expand reimbursement coverage can help drive the broader adoption of bone void fillers and contribute to the growth of the market.

Recent Developments:

|

Development |

Company Name |

|

In May 2021, Medtronic plc acquired Titan Spine, a provider of innovative spinal interbody fusion implants, to expand its portfolio of bone void fillers and enhance its offerings in the spinal fusion market. |

Medtronic plc |

|

In September 2020, Stryker Corporation received FDA approval for its latest generation of bone void fillers, featuring improved design and enhanced biocompatibility for better integration with surrounding bone tissue. |

Stryker Corporation |

|

In March 2022, DePuy Synthes (Johnson & Johnson) announced the launch of a new allograft bone void filler product, leveraging advanced processing techniques to improve its osteoinductive and osteoconductive properties. |

DePuy Synthes (Johnson & Johnson) |

|

In August 2021, Integra LifeSciences Holdings Corporation acquired Surgennes, a French medical device company specializing in bone void fillers and other orthopedic solutions, to strengthen its portfolio and expand its presence in the European market. |

Integra LifeSciences Holdings Corporation |

Market Regional Insights:

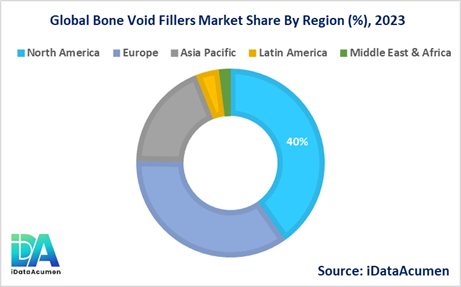

The Bone Void Fillers Market is segmented across various regions, with North America expected to be the largest market during the forecast period, accounting for over 40.2% of the market share in 2024. The growth of the market in North America is attributed to the high prevalence of bone-related disorders, such as osteoporosis, and the presence of well-established healthcare infrastructure that supports the adoption of advanced bone void filler products.

The European market is expected to be the second-largest market for Bone Void Fillers, accounting for over 35.1% of the market share in 2024. The growth of the market in Europe is attributed to the increasing incidence of bone fractures, the aging population, and the availability of reimbursement coverage for bone void filler procedures in several European countries.

The Asia Pacific market is expected to be the fastest-growing market for Bone Void Fillers, with a CAGR of over 18.7% during the forecast period by 2024. The growth of the market in Asia Pacific is attributed to the rising prevalence of bone-related disorders, the improving healthcare infrastructure, and the increasing adoption of advanced medical technologies in emerging economies like China and India.

The Latin American and Middle East & Africa regions are expected to hold smaller market shares, accounting for 4.0% and 2.0% of the global market, respectively, in 2024. However, these regions present growth opportunities as they continue to develop their healthcare systems and increase access to advanced orthopedic treatments.

Market Segmentation:

- By Product Type

- Synthetic Bone Graft Substitutes

- Demineralized Bone Matrix (DBM)

- Allografts

- Bone Morphogenetic Proteins (BMPs)

- Others (Collagen-based, Ceramic-based, etc.)

- By Application

- Spinal Fusion

- Trauma

- Joint Reconstruction

- Dental

- Others (Foot & Ankle, Craniomaxillofacial, etc.)

- By End-User

- Hospitals

- Orthopedic Clinics

- Ambulatory Surgical Centers

- Academic and Research Institutes

- Others (Specialty Clinics, etc.)

- By Material

- Calcium Phosphate

- Collagen

- Bioactive Glass

- Polymers

- Others (Ceramics, Composites, etc.)

- By Form

- Putty

- Gel

- Paste

- Granules

- Others (Strips, Blocks, etc.)

- By Regions

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Market Segment Analysis:

Among the segments identified in Task 6, the Synthetic Bone Graft Substitutes segment is projected to be the fastest-growing in the Bone Void Fillers Market, with a CAGR of 6.8% during the forecast period. This growth is attributed to the increasing adoption of these advanced materials due to their improved biocompatibility, osteoinductive properties, and ability to enhance bone regeneration.

The Spinal Fusion segment is expected to be the largest application segment, accounting for over 40% of the market share in 2024. The growing prevalence of spinal disorders, the rising number of spinal fusion procedures, and the increasing use of bone void fillers to support bone healing in these surgeries are the key factors driving the growth of this segment.

The Hospitals segment is anticipated to be the largest end-user segment, holding a market share of around 50% in 2024. This is due to the higher adoption of bone void fillers in hospital settings, where complex orthopedic procedures are performed, and the availability of advanced healthcare infrastructure to support the use of these medical devices.

Top Companies in the Bone Void Fillers Market:

- Medtronic plc

- Stryker Corporation

- DePuy Synthes (Johnson & Johnson)

- Zimmer Biomet Holdings, Inc.

- Evonik Industries AG

- Integra LifeSciences Holdings Corporation

- Baxter International Inc.

- Graftys

- Arthrex, Inc.

- NuVasive, Inc.

- Wright Medical Group N.V.

- Curasan AG

- ORthoPhor

- Biocomposites Ltd.

- Heraeus Medical GmbH

- Bone Solutions Inc.

- Exactech, Inc.

- Algipharma AS

- TEKNIMED

- Aap Implantate AG