Market Analysis:

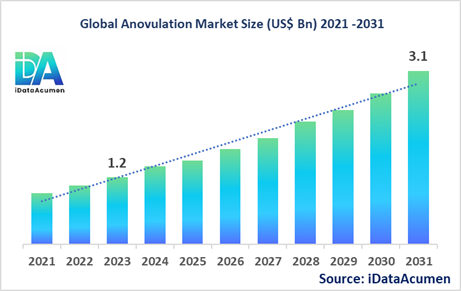

The Anovulation Market had an estimated market size worth US$ 1.2 billion in 2023, and it is predicted to reach a global market valuation of US$ 3.1 billion by 2031, growing at a CAGR of 12.5% from 2024 to 2031.

Anovulation is a condition where a woman's ovaries do not release an egg during her menstrual cycle, which can lead to infertility. Anovulation treatments aim to induce ovulation and increase the chances of conception. These treatments include medications, assisted reproductive technologies (ART), and surgical interventions. The advantages of anovulation treatments include improved fertility outcomes, personalized treatment plans, and advancements in minimally invasive procedures.

Key drivers of the anovulation market include rising infertility rates, increasing awareness about anovulation and its treatment options, and lifestyle changes contributing to infertility.

In summary, the anovulation market focuses on providing treatments and solutions for women experiencing anovulatory cycles, a common cause of infertility.

The Anovulation Market is segmented by treatment type, disease indication, and region. By treatment type, the market is segmented into medication, assisted reproductive technology (ART), surgical intervention, and others (lifestyle modifications, complementary therapies). The medication segment is expected to grow significantly due to the development of new and improved ovulation-inducing drugs, as well as their widespread availability and affordability. Companies like Merck & Co., Inc. and Ferring Pharmaceuticals have recently launched new ovulation-inducing medications, further driving growth in this segment.

Epidemiology Insights:

- The disease burden of anovulation varies across major regions. In North America and Europe, anovulation is a leading cause of infertility, contributing to a significant portion of infertility cases. In contrast, in developing regions like Asia and Africa, anovulation may be overshadowed by other factors contributing to infertility, such as poor access to healthcare and underlying medical conditions.

- Key epidemiological trends and driving factors behind changes in major markets include increasing rates of obesity, polycystic ovary syndrome (PCOS), and advanced maternal age, all of which can contribute to anovulation. Additionally, improved diagnostic techniques and awareness have led to better identification and reporting of anovulation cases.

- In the United States, it is estimated that around 25% of infertile women suffer from anovulation. In Europe, the prevalence of anovulation among infertile women ranges from 15% to 30%, depending on the country. Japan has a relatively lower prevalence of anovulation, estimated at around 10% of infertile women.

- The increasing patient population, particularly in developed regions, presents growth opportunities for the anovulation market. As more women seek fertility treatments and awareness increases, the demand for anovulation treatments is expected to rise.

- Anovulation is not considered a rare disease, as it is a common cause of infertility affecting a significant portion of women of reproductive age.

Market Landscape:

- Unmet needs in the anovulation market include the development of more effective and safer ovulation-inducing medications, as well as improved diagnostics for early detection and monitoring of anovulation.

- Current treatment options for anovulation include medications like clomiphene citrate, letrozole, and gonadotropins, as well as assisted reproductive technologies like in vitro fertilization (IVF) and intrauterine insemination (IUI).

- Upcoming therapies and technologies for anovulation treatment include the development of new ovulation-inducing drugs with fewer side effects, advancements in ovulation prediction and monitoring tools, and improved assisted reproductive techniques.

- Breakthrough treatment options currently in development include the use of stem cell therapy to stimulate ovarian function and the development of gene therapies targeting specific causes of anovulation.

- The anovulation market is dominated by branded drug manufacturers, with a few major pharmaceutical companies holding significant market share. However, there is also a presence of generic drug manufacturers, particularly for older ovulation-inducing medications.

Market Report Scope:

|

Description |

|

|

The market size in 2023 |

US$ 1.2 Bn |

|

CAGR (2024 - 2031) |

12.5% |

|

The revenue forecast in 2031 |

US$ 3.1 Bn |

|

Base year for estimation |

2023 |

|

Historical data |

2019-2023 |

|

Forecast period |

2024-2031 |

|

Quantitative units |

Revenue in USD Million, and CAGR from 2021 to 2030 |

|

Market segments |

|

|

Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East, and Africa |

|

Market Drivers |

|

|

Market Restraints |

|

|

Competitive Landscape |

Merck & Co., Inc., Ferring Pharmaceuticals, Bayer AG, Novartis AG, Pfizer Inc., Sanofi, Myovant Sciences Ltd., AbbVie Inc., Teva Pharmaceutical Industries Ltd., Allergan plc, Gedeon Richter Plc, Mylan N.V., Eli Lilly and Company, Endo International plc, IBSA Institut Biochimique SA, Lupin Limited, Sun Pharmaceutical Industries Ltd., Apotex Inc., Zydus Cadila, Insud Pharma S.L. |

Market Drivers:

Rising Prevalence of Infertility

The increasing prevalence of infertility among women of reproductive age is a significant driver for the anovulation market. Anovulation, which is the absence or irregularity of ovulation, is a leading cause of female infertility. According to the World Health Organization (WHO), infertility affects approximately 48 million couples worldwide. With rising awareness and access to fertility treatments, more women are seeking medical interventions to address anovulation and improve their chances of conceiving. This growing demand for anovulation therapies is fueling the market's growth.

Advancements in Assisted Reproductive Technologies (ART)

Technological advancements in assisted reproductive technologies (ART), such as in vitro fertilization (IVF) and intrauterine insemination (IUI), have revolutionized the treatment of anovulation-related infertility. These techniques offer effective solutions for women struggling with ovulatory disorders, increasing the chances of successful conception. The continuous improvement and development of ART procedures, coupled with their increasing accessibility and affordability, have contributed to the growth of the anovulation market.

Increasing Awareness and Acceptance of Fertility Treatments

Over the past decade, there has been a significant increase in awareness and acceptance of fertility treatments among the general population. Societal attitudes towards infertility and its treatments have shifted, with more open discussions and destigmatization. This change in perception has encouraged more individuals and couples to seek medical assistance for anovulation-related infertility. Awareness campaigns, patient support groups, and improved access to information have played a crucial role in driving the growth of the anovulation market.

Rise in Polycystic Ovary Syndrome (PCOS) and Other Hormonal Imbalances

Polycystic ovary syndrome (PCOS) and other hormonal imbalances that can lead to anovulation are becoming more prevalent, particularly among women of reproductive age. Factors such as sedentary lifestyles, obesity, and environmental factors have contributed to the rise in these conditions. As a result, there is an increasing demand for effective treatments to address anovulation caused by PCOS and other hormonal disorders, driving the growth of the anovulation market.

Market Opportunities:

Personalized Medicine and Precision Diagnostics

Advancements in personalized medicine and precision diagnostics offer significant opportunities for the anovulation market. By leveraging genetic testing, biomarker analysis, and advanced imaging techniques, healthcare providers can develop tailored treatment plans for individual patients. This personalized approach can improve the effectiveness of anovulation treatments, leading to better outcomes and increased patient satisfaction. As research in this field continues, the anovulation market is poised to benefit from the adoption of precision medicine.

Expansion in Emerging Markets

Emerging markets, particularly in Asia and Africa, present a significant growth opportunity for the anovulation market. With improving economic conditions, rising disposable incomes, and increasing access to healthcare services, more women in these regions are seeking fertility treatments. Additionally, governments and healthcare organizations are recognizing the importance of addressing infertility issues, creating favorable policies and initiatives to support the adoption of anovulation therapies. Companies that can effectively tap into these emerging markets have the potential to drive substantial growth in the anovulation market.

Development of Novel Therapeutics

The anovulation market presents opportunities for the development of novel therapeutics with improved efficacy, safety profiles, and fewer side effects. Ongoing research and advancements in fields such as stem cell therapy, gene therapy, and targeted drug delivery systems could lead to breakthrough treatments for anovulation-related infertility. Pharmaceutical companies and research institutions that can successfully develop and commercialize these innovative therapies will have a significant competitive advantage in the anovulation market.

Integration of Digital Technologies

The integration of digital technologies, such as telemedicine, mobile applications, and wearable devices, offers opportunities to enhance the management and treatment of anovulation. These technologies can facilitate remote monitoring, improve patient adherence, and provide personalized guidance throughout the treatment process. Additionally, the use of artificial intelligence (AI) and machine learning algorithms could aid in ovulation prediction, treatment optimization, and better-informed decision-making. Companies that embrace these digital solutions can differentiate themselves and capture a larger share of the anovulation market.

Market Trends:

Increasing Adoption of Minimally Invasive Treatments

The anovulation market is witnessing a trend towards the increased adoption of minimally invasive treatments. Patients and healthcare providers are seeking less invasive and more patient-friendly approaches to address anovulation-related infertility. This trend has driven the development of innovative techniques such as laparoscopic ovarian drilling and endometrial scratching, which offer effective treatments with reduced risks, shorter recovery times, and improved patient comfort.

Focus on Fertility Preservation

As more women delay childbearing due to career or personal preferences, there is a growing focus on fertility preservation techniques. This trend is driven by the increasing awareness of age-related fertility decline and the desire to maintain reproductive options. Techniques like egg freezing (oocyte cryopreservation) and ovarian tissue cryopreservation are gaining traction, enabling women to preserve their fertility for future use. The anovulation market is adapting to meet this demand, offering solutions that support fertility preservation efforts.

Emphasis on Holistic and Complementary Approaches

In addition to conventional medical treatments, there is a growing trend towards the incorporation of holistic and complementary approaches in the management of anovulation. These approaches include lifestyle modifications, dietary changes, stress management techniques, and the use of herbal supplements. Many patients are seeking integrative treatments that address the underlying causes of anovulation and promote overall well-being. Companies in the anovulation market are responding by offering comprehensive solutions that combine conventional therapies with complementary approaches.

Increasing Collaboration and Partnerships

The anovulation market is witnessing a trend towards increased collaboration and partnerships among stakeholders, including pharmaceutical companies, medical device manufacturers, research institutions, and healthcare providers. These collaborations aim to accelerate innovation, share expertise, and develop more effective and comprehensive solutions for anovulation-related infertility. By leveraging collective resources and knowledge, these partnerships can drive advancements in diagnostics, treatments, and patient care, ultimately benefiting the growth of the anovulation market.

Market Restraints:

High Treatment Costs and Limited Access

One of the major restraints in the anovulation market is the high cost of treatments and limited access to fertility services. Assisted reproductive technologies (ART) and advanced anovulation therapies can be financially burdensome for many individuals and couples, especially in regions with limited insurance coverage or lack of government support. Additionally, the availability of specialized fertility clinics and healthcare facilities may be limited in certain geographic areas, further restricting access to anovulation treatments.

Regulatory Challenges and Ethical Concerns

The anovulation market is subject to various regulatory challenges and ethical concerns that can impact its growth. Stringent regulations surrounding the development, approval, and marketing of fertility treatments can prolong the time-to-market for new therapies and increase costs for manufacturers. Additionally, ethical debates surrounding certain assisted reproductive technologies, such as embryo selection or genetic engineering, can create public perception issues and limit their adoption.

Side Effects and Safety Concerns

Many anovulation treatments, particularly hormonal therapies and assisted reproductive technologies, carry the risk of potential side effects and safety concerns. These can include ovarian hyperstimulation syndrome (OHSS), multiple pregnancies, and long-term health implications for both the mother and the child. Such concerns may discourage some patients from pursuing anovulation treatments, limiting the market's growth potential. Ongoing research and development efforts are focused on improving the safety profiles of these treatments to mitigate these restraints.

Recent Developments:

|

Development |

Involved Company |

|

Launched Relugolix in December 2020, a once-daily oral gonadotropin-releasing hormone (GnRH) receptor antagonist for the treatment of endometriosis. |

Myovant Sciences Ltd. |

|

Received FDA approval for Jada System in January 2022, a new in vitro diagnostic device for automated analysis of sperm concentration and motility. |

Esco Medical ApS |

|

Acquired Rebion in December 2021, a company developing ovarian biology platforms to treat infertility and other ovarian disorders. |

OvaScience, Inc. |

|

Product Launch |

Company Name |

|

Launched Letrozole tablets in April 2022, a generic version of the ovulation-inducing drug Femara, used in infertility treatment. |

Teva Pharmaceutical Industries |

|

Received FDA approval for Nextstellis in April 2021, a new combined oral contraceptive for the prevention of pregnancy. |

Mayne Pharma Group Limited |

|

Launched Fertility Blend in October 2020, a dietary supplement designed to support fertility and reproductive health. |

Fairhaven Health, LLC |

|

Merger/Acquisition |

Involved Companies |

|

Acquired Ferring Pharmaceuticals in March 2022, a global leader in reproductive medicine and maternal health. |

Novo Nordisk A/S |

|

Acquired Vitrolife in February 2021, a leading provider of medical devices and services for assisted reproductive technology. |

Cooper Companies, Inc. |

|

Acquired Esco Medical ApS in September 2020, a manufacturer of automated sperm analysis systems for fertility clinics. |

Vitrolife AB |

Market Regional Insights:

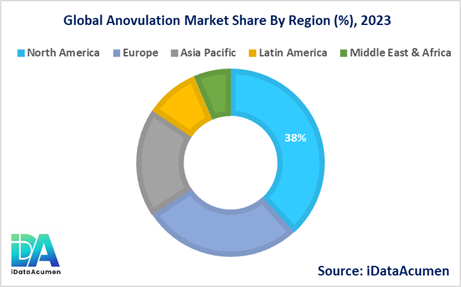

The anovulation market exhibits significant variations across different regions, with distinct drivers and growth prospects. North America is expected to be the largest market for the Anovulation Market during the forecast period, accounting for over 38.2% of the market share in 2024. The growth of the market in North America is attributed to the increasing prevalence of infertility, advanced healthcare infrastructure, and a substantial number of fertility clinics and specialized centers.

The Europe market is expected to be the second-largest market for the Anovulation Market, accounting for over 27.5% of the market share in 2024. The growth of the market is attributed to the rising awareness about infertility treatments, supportive reimbursement policies, and the presence of leading pharmaceutical and medical device companies in the region.

The Asia-Pacific market is expected to be the fastest-growing market for the Anovulation Market, with a CAGR of over 18.7% during the forecast period by 2024. The growth of the market in the Asia-Pacific region is attributed to the increasing adoption of advanced fertility treatments, improving healthcare infrastructure, and a growing patient population. Additionally, the rising disposable incomes and the desire for parenthood in countries like China and India are driving market growth in this region.

Market Segmentation:

- By Treatment Type

- Medication

- Assisted Reproductive Technology (ART)

- Surgical Intervention

- Others (Lifestyle Modifications, Complementary Therapies)

- By Disease Indication

- Polycystic Ovary Syndrome (PCOS)

- Hypothalamic Amenorrhea

- Premature Ovarian Failure

- Hyperprolactinemia

- Thyroid Disorders

- Others (Obesity, Aging, Idiopathic)

- By Route of Administration

- Oral

- Injectable

- Implants

- Others (Transdermal, Vaginal)

- By End-user

- Hospitals

- Fertility Clinics

- Academic and Research Institutes

- Others (Home Care, Gynecology Centers)

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Others (Direct Tenders, Specialty Clinics)

- By Regions

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Market Segment Analysis:

- By Treatment Type: The medication segment is expected to grow significantly across all regions, driven by the development of new and improved ovulation-inducing drugs. In North America and Europe, this segment is projected to have a CAGR of around 10-12% and a market size of $800 million-$1 billion by 2024. The assisted reproductive technology (ART) segment is also anticipated to grow rapidly, particularly in regions with advanced healthcare infrastructure and increasing adoption of fertility treatments, such as North America and Europe.

- By Disease Indication: The polycystic ovary syndrome (PCOS) segment is likely to be the largest and fastest-growing segment across regions. In North America and Europe, this segment is expected to have a CAGR of around 12-15% and a market size of $600 million-$800 million by 2024. The hypothalamic amenorrhea segment is also projected to witness significant growth, particularly in Asia-Pacific, due to increasing awareness and changing lifestyles.

- By Region: North America is expected to remain the largest market for anovulation treatments, driven by advanced healthcare infrastructure, high adoption rates, and favorable reimbursement policies. The Asia-Pacific region is anticipated to be the fastest-growing market, with a CAGR of around 15-18%, due to increasing disposable incomes, improving healthcare facilities, and a growing patient population.

Top Companies in the Anovulation Market:

- Merck & Co., Inc.

- Ferring Pharmaceuticals

- Bayer AG

- Novartis AG

- Pfizer Inc.

- Sanofi

- Myovant Sciences Ltd.

- AbbVie Inc.

- Teva Pharmaceutical Industries Ltd.

- Allergan plc

- Gedeon Richter Plc

- Mylan N.V.

- Eli Lilly and Company

- Endo International plc

- IBSA Institut Biochimique SA

- Lupin Limited

- Sun Pharmaceutical Industries Ltd.

- Apotex Inc.

- Zydus Cadila

- Insud Pharma S.L.