Market Analysis:

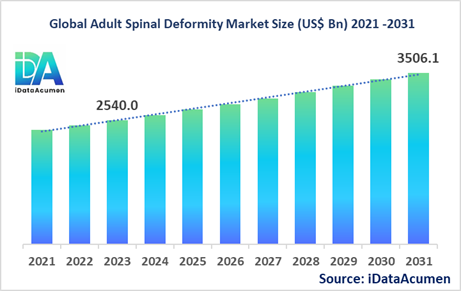

The Adult Spinal Deformity Market had an estimated market size worth US$ 2,540.3 million in 2023, and it is predicted to reach a global market valuation of US$ 3,506.1 million by 2031, growing at a CAGR of 4.11% from 2024 to 2031.

Adult spinal deformities are abnormal curvatures or alignments of the spine that can occur in adults due to various factors such as aging, injury, or underlying conditions. These deformities can lead to pain, reduced mobility, and other health complications. Spinal fusion devices, spinal osteotomy devices, and spinal correction and deformity devices are some of the key products used in the treatment of adult spinal deformities.

The major drivers for the adult spinal deformity market include the growing geriatric population and the increasing prevalence of spinal deformities. According to the World Health Organization, the global population aged 60 years and above is expected to reach 2.1 billion by 2050, up from 900 million in 2015, which is likely to drive the demand for effective treatment options.

In summary, the Adult Spinal Deformity Market is a crucial segment of the medical devices industry, focused on addressing the growing need for advanced treatments and technologies to manage spinal deformities in adults. The market is segmented by product type, procedure, end-user, technology, and application, with the spinal fusion devices segment expected to be a key contributor to the market's growth.

The Adult Spinal Deformity Market is segmented by product type, procedure, end-user, technology, and application. By product type, the market is segmented into spinal fusion devices, spinal osteotomy devices, spinal correction and deformity devices, spinal arthrodesis devices, spinal fixation devices, and spinal biologics. The spinal fusion devices segment is one of the largest subsegments, as these devices are widely used in the treatment of spinal deformities to stabilize and align the spine. Companies in the market are continuously developing innovative fusion devices to improve patient outcomes.

Epidemiological Insights:

Disease Burden Across Regions: The burden of adult spinal deformities is significant globally, with North America and Europe accounting for the highest prevalence. In the United States, it is estimated that around 8-10% of adults suffer from some form of spinal deformity, while in Europe, the prevalence is around 6-8%.

Key Epidemiological Trends: The key epidemiological trends driving the growth of the adult spinal deformity market include the aging population, increasing rates of obesity, and the rising incidence of trauma and sports-related injuries. The growing prevalence of degenerative spinal conditions, such as scoliosis and kyphosis, is also a significant factor.

Disease Incidence and Prevalence: In the United States, the prevalence of adult scoliosis is estimated to be around 6%, while the prevalence of adult kyphosis is approximately 4%. In Europe, the prevalence of adult scoliosis is around 4-6%, and the prevalence of adult kyphosis is 3-5%.

Growth Opportunities: The increasing awareness about spinal deformities and the availability of advanced treatment options are expected to drive the growth opportunities for the adult spinal deformity market. Additionally, the rising focus on early diagnosis and preventive care can also contribute to the market's growth.

Rare Disease Aspects: Adult spinal deformities are not considered rare diseases, as they affect a significant portion of the adult population. However, certain underlying genetic or congenital conditions that can lead to spinal deformities, such as Marfan syndrome or Ehlers-Danlos syndrome, are relatively rare.

Market Landscape:

Unmet Needs: The adult spinal deformity market still has several unmet needs, including the development of more effective and minimally invasive surgical techniques, the need for personalized treatment options, and the improvement of long-term outcomes for patients.

Current Treatment Options: The current treatment options for adult spinal deformities include conservative therapies, such as physical therapy and bracing, as well as surgical interventions, including spinal fusion, osteotomy, and deformity correction procedures. Approved therapies in the market include a range of spinal implants, biologics, and minimally invasive surgical tools.

Upcoming Therapies and Technologies: The market is witnessing the development of several promising upcoming therapies and technologies, such as advanced spinal correction devices, robotic-assisted surgical systems, and the integration of digital technologies like 3D printing and artificial intelligence for personalized treatment planning.

Breakthrough Treatment Options: One of the key breakthrough treatment options currently being developed is the use of regenerative medicine, including stem cell therapies and tissue engineering approaches, to promote spinal fusion and aid in the repair of spinal deformities.

Market Composition: The adult spinal deformity market is relatively consolidated, with a few large players, such as Medtronic, Stryker, and DePuy Synthes, dominating the market. However, there is also a presence of smaller, specialized companies focused on developing innovative solutions for the treatment of spinal deformities.

Market Report Scope:

|

Description |

|

|

The market size in 2023 |

US$ 2,540.3 Mn |

|

CAGR (2024 - 2031) |

4.11% |

|

The revenue forecast in 2031 |

US$ 3,506.1 Mn |

|

Base year for estimation |

2023 |

|

Historical data |

2019-2023 |

|

Forecast period |

2024-2031 |

|

Quantitative units |

Revenue in USD Million, and CAGR from 2021 to 2030 |

|

Market segments |

|

|

Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East, and Africa |

|

Market Drivers |

|

|

Market Restraints |

|

|

Competitive Landscape |

Medtronic plc, Stryker Corporation, DePuy Synthes (Johnson & Johnson), Zimmer Biomet Holdings, Inc., Globus Medical, Inc., NuVasive, Inc., K2M Group Holdings, Inc. (Stryker), Alphatec Holdings, Inc., Spine Wave, Inc., Exactech, Inc., SeaSpine Holdings Corporation, RTI Surgical Holdings, Inc., Orthofix Medical Inc., Spinal Elements, Inc., Medacta International, Simplify Medical, Inc., Premia Spine Ltd., Kuros Biosciences AG, Colfax Corporation (DJO Global), Innovasis, Inc. |

Market Drivers:

Increasing Prevalence of Spinal Deformities in the Aging Population

The growing geriatric population is a significant driver for the adult spinal deformity market. As individuals age, the risk of developing spinal deformities, such as scoliosis, kyphosis, and degenerative disc disease, increases. According to the World Health Organization, the global population aged 60 years and above is expected to reach 2.1 billion by 2050, up from 900 million in 2015. This aging demographic is more susceptible to acquiring spinal deformities, leading to a surge in the demand for effective treatment options. Additionally, the rising prevalence of lifestyle-related factors, such as obesity and sedentary behaviors, can contribute to the development of spinal deformities in the adult population, further driving the need for advanced spinal care solutions.

Advancements in Surgical Techniques and Medical Technologies

The adult spinal deformity market has witnessed significant advancements in surgical techniques and medical technologies, which have contributed to the growth of the market. The introduction of minimally invasive surgical procedures, such as endoscopic spinal fusion and robotic-assisted surgeries, has improved patient outcomes, reduced recovery times, and increased the adoption of these treatments. These innovative techniques offer greater precision, better visualization of the surgical site, and reduced tissue trauma, making them an attractive option for both healthcare providers and patients. Furthermore, the integration of digital technologies, such as 3D printing, computer-assisted planning, and real-time intraoperative navigation, has enhanced the accuracy and personalization of spinal deformity treatments, driving the adoption of these advanced solutions.

Increasing Awareness and Improved Diagnosis of Spinal Deformities

The growing awareness about adult spinal deformities, coupled with the availability of improved diagnostic tools, is another key driver for the market. Advancements in imaging technologies, such as MRI, CT scans, and digital X-rays, have enabled more accurate and earlier detection of spinal deformities, leading to timely interventions and improved patient outcomes. Healthcare providers are also becoming more proactive in screening for spinal deformities, particularly among the elderly population, as early detection can significantly impact the course of treatment and long-term patient prognosis. The increased focus on preventive care and the availability of specialized spinal deformity clinics have further contributed to the rising awareness and diagnosis of these conditions.

Expansion of Healthcare Infrastructure and Reimbursement Coverage

The expansion of healthcare infrastructure, particularly in emerging markets, is driving the growth of the adult spinal deformity market. Governments and healthcare authorities are investing in the development of modern medical facilities, specialized treatment centers, and skilled healthcare professionals to address the increasing demand for spinal care. Additionally, the availability of reimbursement coverage for spinal deformity treatments, both through public and private insurance schemes, has improved patient access to these specialized interventions. This factor has been particularly relevant in developed markets, where reimbursement policies have been more favorable, enabling more patients to seek and receive the necessary treatments.

Market Opportunities:

Expansion into Emerging Markets

The adult spinal deformity market presents significant growth opportunities in emerging markets, such as Asia Pacific, Latin America, and the Middle East & Africa. These regions are characterized by rapidly aging populations, increasing prevalence of spinal deformities, and expanding healthcare infrastructure. As these markets continue to develop, the demand for advanced spinal care solutions is expected to rise. Companies in the adult spinal deformity market can capitalize on this opportunity by establishing a strong presence in these regions, partnering with local healthcare providers, and tailoring their product offerings to meet the unique needs of the respective patient populations. Additionally, the development of affordable and accessible treatment options can further drive market penetration in these emerging markets.

Integration of Digital Technologies and Personalized Treatments

The integration of digital technologies, such as 3D printing, artificial intelligence, and augmented reality, offers tremendous opportunities for the adult spinal deformity market. These innovations can enable the development of personalized spinal implants, patient-specific surgical planning, and real-time guidance during complex procedures. By leveraging these advanced technologies, healthcare providers can deliver more precise and tailored treatments, improving surgical outcomes and enhancing patient satisfaction. Furthermore, the incorporation of data analytics and predictive modeling can aid in identifying high-risk patients, optimizing treatment strategies, and enhancing long-term patient monitoring and care. This shift towards personalized medicine can significantly improve the quality of life for individuals suffering from adult spinal deformities.

Advancements in Regenerative Medicine and Biologics

The field of regenerative medicine and the use of biological therapies present promising opportunities for the adult spinal deformity market. Emerging technologies, such as stem cell therapies, tissue engineering, and the application of growth factors, have the potential to promote spinal fusion, facilitate the repair of deformities, and potentially reverse the progression of certain spinal conditions. These innovative approaches can offer alternative treatment options for patients, particularly those who may not be suitable candidates for traditional surgical interventions. As the understanding of spinal biology and the mechanisms of deformity progression continue to evolve, the integration of regenerative medicine solutions can revolutionize the management of adult spinal deformities, leading to improved clinical outcomes and reduced long-term complications.

Expansion of Minimally Invasive Surgical Techniques

The growing adoption of minimally invasive surgical techniques for the treatment of adult spinal deformities presents a significant opportunity for market growth. These advanced procedures, such as endoscopic spinal fusion and percutaneous osteotomies, offer numerous benefits, including reduced surgical trauma, faster recovery times, and lower rates of complications. As healthcare providers and patients become more aware of the advantages of minimally invasive approaches, the demand for these specialized surgical solutions is expected to rise. Companies in the adult spinal deformity market can capitalize on this trend by developing innovative instruments, implants, and surgical systems designed specifically for minimally invasive spinal interventions. The expansion of minimally invasive techniques can enhance patient outcomes, increase the accessibility of spinal deformity treatments, and drive the overall growth of the market.

Market Trends:

Shift towards Patient-Centric and Outcome-Driven Care

The adult spinal deformity market is witnessing a shift towards a more patient-centric and outcome-driven approach to care. Healthcare providers and medical device manufacturers are increasingly focusing on developing solutions that prioritize patient preferences, improve quality of life, and deliver better long-term outcomes. This trend is evidenced by the growing emphasis on shared decision-making, the incorporation of patient-reported outcome measures, and the development of personalized treatment plans. By aligning their offerings with the specific needs and expectations of adult spinal deformity patients, companies can enhance treatment adherence, patient satisfaction, and overall clinical success rates. Additionally, the integration of digital technologies, such as wearable devices and mobile applications, can enable continuous patient monitoring and facilitate the collection of real-world data to further optimize care delivery.

Increasing Adoption of Minimally Invasive Surgical Techniques

The adult spinal deformity market is witnessing a significant trend towards the adoption of minimally invasive surgical techniques. These advanced procedures, such as endoscopic spinal fusion and robotic-assisted surgeries, offer several advantages over traditional open surgical approaches, including reduced tissue trauma, shorter hospital stays, and faster recovery times. As healthcare providers and patients become more aware of the benefits of minimally invasive interventions, the demand for these specialized surgical solutions is expected to rise. Companies in the adult spinal deformity market are responding to this trend by developing innovative instruments, implants, and navigational systems specifically designed for minimally invasive procedures. The expansion of minimally invasive techniques can enhance patient outcomes, increase the accessibility of spinal deformity treatments, and drive the overall growth of the market.

Emphasis on Preventive Care and Early Intervention

The adult spinal deformity market is also experiencing a growing emphasis on preventive care and early intervention strategies. Healthcare providers are becoming more proactive in screening for spinal deformities, particularly among the elderly population and individuals with underlying risk factors. The availability of improved diagnostic tools, such as advanced imaging technologies and computerized spinal assessments, has enabled earlier detection of spinal abnormalities, allowing for timely interventions and potentially preventing the progression of deformities. Additionally, the development of educational campaigns and the implementation of specialized spinal health programs can promote awareness among the general public, encouraging individuals to seek early evaluation and adopt preventive measures. By focusing on preventive care and early intervention, the market can potentially reduce the overall burden of adult spinal deformities and improve patient outcomes.

Increasing Focus on Comprehensive Spinal Care Solutions

The adult spinal deformity market is also witnessing a trend towards the provision of comprehensive spinal care solutions. Healthcare providers and medical device companies are recognizing the importance of addressing the holistic needs of patients with spinal deformities, rather than focusing solely on surgical interventions. This integrated approach encompasses a range of services, including pre-operative planning, intraoperative navigation, post-operative rehabilitation, and long-term follow-up care. By offering a continuum of care, companies can enhance the overall patient experience, improve clinical outcomes, and reduce the risk of complications. Furthermore, the integration of digital technologies, such as patient portals and telehealth solutions, can further strengthen the delivery of comprehensive spinal care, enabling remote monitoring, virtual consultations, and seamless coordination among healthcare professionals.

Market Restraints:

High Cost of Spinal Deformity Treatments

One of the significant restraints in the adult spinal deformity market is the high cost of treatments, which can limit patient access and affordability. Spinal deformity interventions, particularly complex surgical procedures, often involve the use of advanced medical devices, specialized surgical instruments, and extensive hospital stays, leading to significant financial burdens for patients and healthcare systems. The high costs associated with these treatments can be a barrier, especially in regions with limited healthcare coverage or inadequate reimbursement policies. This restraint can disproportionately impact underserved populations and vulnerable patient groups, restricting their ability to access the necessary care. Addressing the affordability of spinal deformity treatments through innovative financing models, strategic partnerships, and policy-level interventions can help overcome this key market restraint.

Complications and Risks Associated with Spinal Surgeries

The adult spinal deformity market is also constrained by the inherent risks and complications associated with spinal surgical interventions. Procedures to correct spinal deformities, such as spinal fusion, osteotomy, and deformity correction, carry the potential for serious complications, including neurological injuries, bleeding, infection, and hardware-related issues. These risks can lead to longer recovery times, increased morbidity, and even mortality in some cases. Healthcare providers and patients often have to weigh the potential benefits of surgical treatment against the associated risks, which can be a barrier to the widespread adoption of these interventions. Continuous advancements in surgical techniques, improved patient selection criteria, and the development of minimally invasive procedures can help mitigate these risks and address this key restraint in the adult spinal deformity market.

Limited Access to Specialized Spinal Care in Certain Regions

Another significant restraint in the adult spinal deformity market is the limited access to specialized spinal care in certain regions, particularly in developing and underserved areas. The availability of healthcare infrastructure, skilled healthcare professionals, and advanced medical technologies may be scarce in these regions, making it challenging for patients to receive the necessary treatment for their spinal deformities. This geographical disparity in access to specialized care can lead to delayed diagnoses, suboptimal treatment, and worsening of patient outcomes. Addressing this restraint requires a multi-pronged approach, including investments in healthcare infrastructure, training of specialized healthcare providers, and the implementation of telemedicine solutions to improve the reach and accessibility of spinal deformity care in underserved regions.

Recent Developments:

|

Development |

Company Name |

|

In March 2023, Medtronic received FDA approval for its Solera Tkd Spinal System, a comprehensive solution for the treatment of adult spinal deformities. The system offers improved surgical flexibility and enhanced patient outcomes. |

Medtronic |

|

In September 2022, Stryker launched its Inertia Spinal System, a next-generation spinal correction and deformity system designed to address complex adult spinal deformities. The system utilizes advanced technologies to provide more precise and customizable surgical solutions. |

Stryker |

|

In July 2021, DePuy Synthes, a Johnson & Johnson company, acquired Orthotaxy, a developer of software-enabled surgery technologies, to further enhance its capabilities in the treatment of adult spinal deformities. The acquisition will enable DePuy Synthes to integrate advanced digital solutions into its spinal deformity portfolio. |

DePuy Synthes (Johnson & Johnson) |

|

In February 2022, Globus Medical received FDA clearance for its ExcelsiusGPS Robotic Navigation System, which allows for more accurate and minimally invasive surgical treatments for adult spinal deformities. The system combines robotic guidance with advanced imaging technology to improve surgical precision. |

Globus Medical |

|

In October 2021, NuVasive announced the launch of its Reline 3D system, a comprehensive solution for the surgical correction of adult spinal deformities. The system incorporates the latest advancements in spinal implants and instrumentation to enhance surgical precision and patient outcomes. |

NuVasive |

Market Regional Insights:

Adult Spinal Deformity Market Regional Insights Overview: The adult spinal deformity market is a global industry, with significant growth opportunities across various regions. The market is analyzed based on five major geographical regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

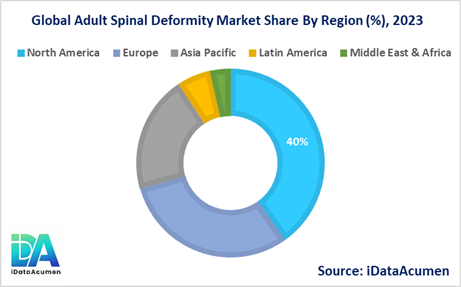

North America: North America is expected to be the largest market for the Adult Spinal Deformity Market during the forecast period, accounting for over 40% of the market share in 2024. The growth of the market in North America is attributed to the high prevalence of spinal deformities, the presence of advanced healthcare infrastructure, and the availability of reimbursement coverage for spinal deformity treatments.

Europe: The European market is expected to be the second-largest market for the Adult Spinal Deformity Market, accounting for over 30% of the market share in 2024. The growth of the market in Europe is attributed to the increasing geriatric population, the rising awareness about spinal deformities, and the improving access to advanced spinal care.

Asia Pacific: The Asia Pacific market is expected to be the fastest-growing market for the Adult Spinal Deformity Market, with a CAGR of over 20% during the forecast period by 2024. The growth of the market in the Asia Pacific region is attributed to the increasing prevalence of spinal deformities, the improving healthcare infrastructure, and the growing medical tourism industry.

Latin America and the Middle East & Africa: These regions are expected to have a relatively smaller market share compared to North America, Europe, and the Asia Pacific. However, the markets in these regions are expected to experience steady growth due to the increasing awareness about spinal deformities and the expansion of healthcare services.

Market Segmentation:

- By Product Type

- Spinal Fusion Devices

- Spinal Osteotomy Devices

- Spinal Correction and Deformity Devices

- Spinal Arthrodesis Devices

- Spinal Fixation Devices

- Spinal Biologics

- Others (ex. Spinal Braces, Spinal Traction Devices)

- By Procedure

- Spinal Fusion Surgery

- Osteotomy

- Spinal Deformity Correction

- Spinal Arthrodesis

- Spinal Fixation

- Minimally Invasive Spinal Surgeries

- Others (ex. Spinal Bracing, Spinal Traction)

- By Regions

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Segments Analysis:

Spinal Fusion Devices Segment: The spinal fusion devices segment is expected to be the largest and fastest-growing segment in the adult spinal deformity market. This is due to the increasing prevalence of spinal deformities, the rising adoption of advanced fusion technologies, and the growing demand for minimally invasive surgical options. The spinal fusion devices segment is projected to grow at a CAGR of 4.3% from 2024 to 2031, reaching a market size of US$ 3,107.0 million by 2031.

Minimally Invasive Spinal Surgeries Segment: The minimally invasive spinal surgeries segment is another key growth area in the adult spinal deformity market. This segment is expected to grow at a CAGR of 4.1% from 2024 to 2031, driven by the advantages of these techniques, such as reduced patient recovery time, lower risk of complications, and improved surgical precision. The market size for minimally invasive spinal surgeries is expected to reach US$ 2,866.6 million by 2031.

Spinal Biologics Segment: The spinal biologics segment, which includes technologies like stem cell therapies and tissue engineering, is a rapidly evolving area in the adult spinal deformity market. This segment is expected to grow at a CAGR of 3.8% from 2024 to 2031, as these innovative therapies offer the potential to promote spinal fusion and facilitate the repair of spinal deformities. The market size for spinal biologics is projected to reach US$ 2,644.7 million by 2031.

Top Companies in the Adult Spinal Deformity Market

- Medtronic plc

- Stryker Corporation

- DePuy Synthes (Johnson & Johnson)

- Zimmer Biomet Holdings, Inc.

- Globus Medical, Inc.

- NuVasive, Inc.

- K2M Group Holdings, Inc. (Stryker)

- Alphatec Holdings, Inc.

- Spine Wave, Inc.

- Exactech, Inc.

- SeaSpine Holdings Corporation

- RTI Surgical Holdings, Inc.

- Orthofix Medical Inc.

- Spinal Elements, Inc.

- Medacta International

- Simplify Medical, Inc.

- Premia Spine Ltd.

- Kuros Biosciences AG

- Colfax Corporation (DJO Global)

- Innovasis, Inc.